Resale HDB Flat Buying Guide: 5 Things to Do Beforehand

FYI for anyone interested in purchasing a pre-loved flat in Singapore.

BTO proposals are so often joked about that they have become part and parcel of Singaporean culture. But there is always a good explanation as to why they are such a popular (though somewhat cliché) reason for popping the marriage question: personal space, or more specifically, a home that a newlywed couple can call their own, is essential for a healthy relationship.

However, for married couples who are eager to move in together, the wait time of 3 to 5 years for the construction of a BTO flat may be too long – which brings them to the decision of purchasing a resale HDB flat off the open market instead.

To help you ease into the process, here are 5 to-dos covering various aspects of purchasing a resale HDB home in Singapore, from house hunting to applying for grants!

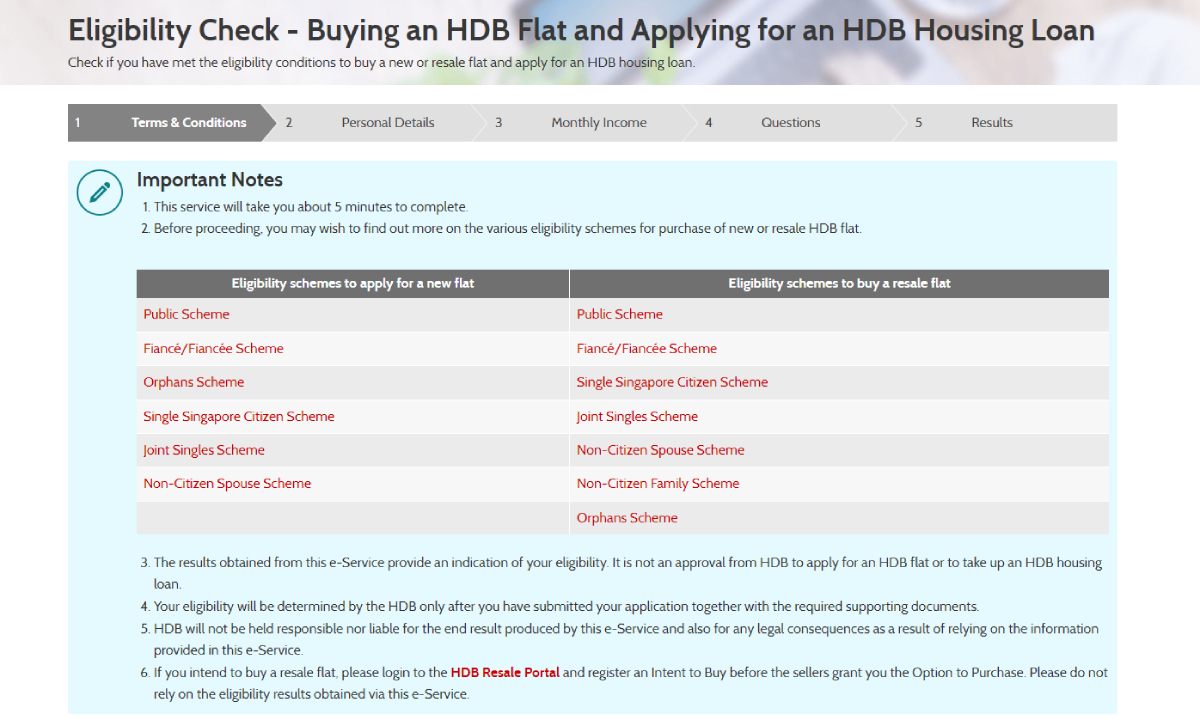

1. Find out the eligibility schemes necessary to purchase an HDB resale flat

HDB flats are built with the intention of providing quality, affordable housing for Singaporeans, so it stands to reason that there are various prerequisites that must be met in order to be an eligible buyer.

The quickest way to know if you satisfy the necessary requirements to buy a resale flat is by completing a simple online assessment on HDB’s homepage, which will also assess your eligibility for an HDB housing loan and grants.

Additionally, you should be aware of the eligibility schemes for purchasing an HDB resale flat. The reason for this is that in order to establishing qualifying conditions, these schemes also have an impact on the benefits available to interested buyers, and even the types of resale HDB flats they can purchase.

For instance, unlike resale HDB flat buyers who fall under the Public Scheme, those applying under the Single Singapore Citizen Scheme are unable to purchase 3-Gen units.

Below is a table summarising the key requirements for each Resale HDB Flat Eligibility Scheme:

| Resale HDB Flat Eligibility Scheme | Who Falls Under It? | Notable Scheme Requirements |

| Public Scheme | Wedded couples, families with children | - Applicant must be a Singapore Citizen (SC) or Singapore Permanent Resident (SPR). - At least one listed occupier must be a SC or SPR. |

| Fiancé/Fiancée Scheme | Engaged, unwedded couples | - All applicants must either be a SC or SPR. - Marriage must be solemnised within 3 months of completion of flat purchase. |

| Single Singapore Citizen Scheme | Singles | - Applicant must be a SC. - If unmarried, applicant must be > 35 years old. - If widowed or orphaned, applicant must be > 21 years old. |

| Joint Singles Scheme | For groups of 2 to 4 singles | - All applicants must be SCs and single. - Same age requirements as Single Singapore Citizen Scheme apply to applicants.

|

| Non-Citizen Spouse Scheme | Couples with a non-local spouse | - Applicant must be an SC. - If applicant is 21 years old and above, spouse must have a valid Long-Term Visit Pass (LTVP) or Work Pass (WP) of at least 6 months when purchase application is submitted.

- If applicant is 35 years old and above, spouse will too need a Valid LTVP or WP when a purchase application is made, but of any validity period. |

| Non-Citizen Family Scheme | Family with a non-local member(s) | - At least one non-SC parent, sibling, or child has to be included in the application. - At least 1 parent or child must have a valid LTVP or WP of at least 6 months when purchase application is submitted. |

| Orphans Scheme | Single orphan siblings | - All siblings must be named in the same application, single, and are not applying, owning or renting a flat separately. - At least one of the applicant’s deceased parents must have been be a SC or SPR. |

In addition to the conditions listed above, there are other criteria that apply regardless of which resale HDB flat eligibility scheme you qualify under. These requirements include:

- Ownership or interest in other local and/or overseas properties

If the applicant and/or any person(s) listed in a resale flat application has an interest and/or ownership in another local and/or overseas property (including currently-owned HDB flats), they are required to dispose of the said property within 6 months of completing the resale flat’s purchase.

- The Ethnic Integration Policy (EIP) and Singapore PR Quota

Depending on the EIP and/or SPR quotas of a specific block or neighbourhood, you may be unable to buy a resale HDB flat in the area.

For a thorough explanation of every eligibility scheme and its requirements, check out HDB’s official site here.

2. Look into the types of HDB grants that are available

HDB housing grants (or CPF housing grants) are a form of financial assistance, given to help Singapore residents acquire a home of their own. And how exactly they work is also straightforward – these grants can be used to offset the purchase price of a resale (or new) HDB flat, hence lowering the amount of money a buyer needs to take out on a home loan.

What is slightly complex, though, are the types of grants applicable to each HDB Flat Eligibility Scheme when purchasing a resale flat:

| Resale HDB Flat Eligibility Scheme | Possible Applicable Grants When Buying a Resale HDB Flat |

| Public Scheme | - CPF Housing Grant (Families) - Enhanced CPF Housing Grant (Families) - Step-Up Housing Grant (Families) - Proximity Housing Grant (Families) |

| Fiancé/Fiancée Scheme | Same as Public Scheme.

|

| Single Singapore Citizen Scheme | - CPF Housing Grants (Singles)

|

| Joint Singles Scheme | Same as Single Singapore Citizen Scheme.

|

| Non-Citizen Spouse Scheme | Same as Single Singapore Citizen Scheme.

|

| Non-Citizen Family Scheme | Same as Single Singapore Citizen Scheme.

|

| Orphans Scheme | - CPF Housing Grants (Singles)

|

Do also take note that certain conditions have to be met by you (and/or your family) in order to qualify for these grants when buying a resale HDB flat.

One example would be the lease requirement for Enhanced Housing Grants, which singles and families can apply for, only if the remaining lease on their ideal resale flat is 20 years or more.

| Type of Grant | Grant Amount for First-Timer Families | Grant Amount for First-Timer Singles |

| CPF Housing Grant | Up to $50,000 (for 4-room or smaller resale flats)

Up to $40,000 (for 5-room or larger resale flats)

| Up to $25,000 (for 4-room or smaller resale flats)

Up to $20,000 (for 5-room or larger resale flats)

|

| Enhanced CPF Housing Grant | Up to $80,000 | Up to $40,000 |

| Proximity Housing Grant | Up to $30,000 | Up to $15,000 |

More details about qualifying requirements, as well as receivable amounts for HDB’s single and family housing grants, can be found here and here respectively.

3. Tap on online tools for market research and financial planning

Just like how you would take a look at the price tags on groceries or clothing before adding them to your shopping cart, having an idea of how much you will be forking out for an HDB resale flat is essential – if not for financial planning, then for general awareness.

And one resource that allows you to do just that is the official HDB resale flat price checker, which will give you an idea of how much a resale flat will cost in your desired neighbourhood.

Although they serve a different purpose, HDB’s online financial calculators are also valuable resources worth bookmarking. These include the:

When used in tandem, these calculators should give you a comprehensive view of your finances while guiding your purchasing decisions, which brings us to…

4. Looking into the types of home loans available

Given the high prices of HDB resale flats and the length of time required to repay borrowed credit (typically decades), homebuyers must carefully consider their housing loan options before signing on the dotted line.

Loans for resale HDB flats can be broadly categorised into two types, bank loans and HDB loans, which are summarised below:

| Bank Loans for Resale HDB Flats | HDB Loans for Resale HDB Flats | |

| Interest Rate | Varies by bank, changes according to the market. | Pegged at 0.1% above the prevailing CPF Ordinary Account interest rate. |

| Max. Repayment Period | Up to 30 years. | Capped at whichever is the shortest: - 25 years - Up till buyer is 65 y/o - Remaining lease of flat minus 20 years. |

| Loan-to-Value (LTV) Limit | Up to 75% of resale price or value of the flat, whichever is lower. | Up to 80% of resale price or value of the flat, whichever is lower.

|

Monthly Instalments

| Capped at 30% of buyers’ gross monthly income. | Capped at 30% of buyers’ gross monthly income. |

CPF Utilisation Allowed?

| Yes. | Yes. |

5. Get familiarised with the necessary steps and payments

Knowing when to start paying for your resale flat is just as important as knowing how much you will be forking out for it. And for this reason, it is highly-recommended for to-be homebuyers to familiarise themselves with the resale flat purchasing process as much as possible.

| Stage of Buying Process | Actions Required |

| Register Intent to Buy | - Register an Intent to Buy, after which you will be assessed for your eligibility to buy a resale flat, housing grant(s), as well as an HDB housing loan.

|

| Obtain Option to Purchase (OTP) from Seller | - Look for a suitable resale HDB flat and obtain an OTP from the buyer.

|

| Decide Between HDB or Bank Loan | - For HDB loans, you will need a valid HDB Loan Eligibility Letter before the OTP is granted.

|

| Submit Request for Value | - Submit a Request for Value, which will determine the flat’s value, and in turn, your CPF usage and housing loan amount.

|

| Exercise OTP | - Proceed with the flat purchase by exercising the OTP.

- At this stage, you will need to pay the Option Exercise Fee*, which when including the Option Fee* must be < $5,000.

(*Option Fee + Option Exercise Fee = Deposit)

|

| Submit Resale Application | - Both homebuyers and sellers have to submit their respective halves of the resale application within 7 calendar days.

|

| Endorse Documents and Pay Fees | - HDB will prepare the necessary documents for endorsement approx. 3 weeks after the Resale Application has been accepted.

- For HDB loans, the Initial Payment will be 15% of the resale price or value of the flat, whichever is lower. - For bank loans, assuming an LTV limit of 75%, the Initial Payment will be 25% of resale price or value of the flat, whichever is lower.

|

| Get Resale Approval | - Once all fees are paid, an in-principle approval will be issued by HDB and the resale application will be processed.

|

| Attend Completion Appointment | - 8 weeks from the resale application’s date of acceptance, buyers and sellers will be invited to complete the transaction in-person at the HDB Resale Office at HDB Hub. |

And with that, here is everything you will need to do and take note of as a first-time resale HDB flat buyer.

Also, if you require professional advice to kickstart your home buying/selling journey, don’t hesitate to reach out to any of our trusted ERA advisors!

Disclaimer for consumer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.