High-for-Longer Interest Rates Will Persist, But Buying a Home Now May Still Pay Off Later

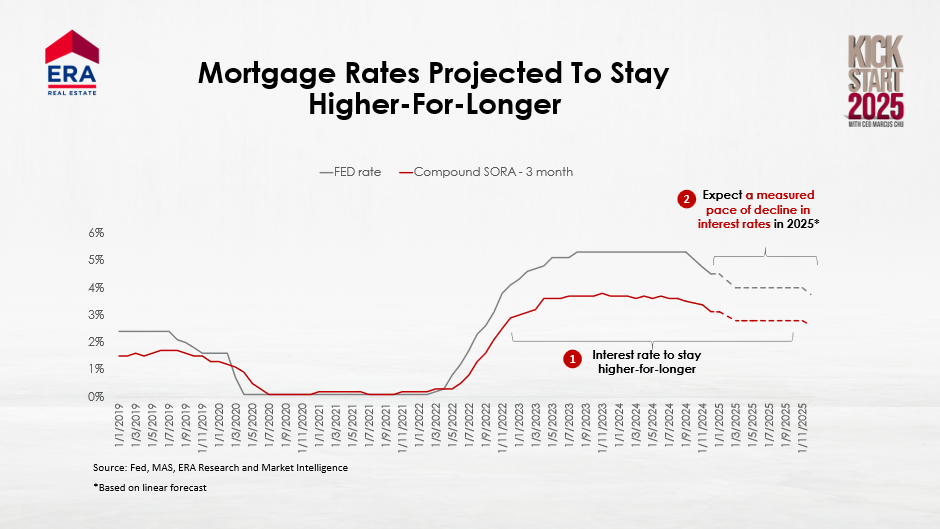

Following a prolonged cycle of elevated interest rates beginning in 2022, the U.S. Federal Reserve finally announced its first rate cut in September last year. This reduction of 50 basis points was followed by two subsequent rounds of rate cuts, which saw the federal funds rate reduced twice by 25 basis points in November and December 2024.

These cuts also resulted in the Fed’s target rate being brought down to between 4.25% and 4.5% by end-2024. Locally, the three-month compounded Singapore Overnight Rate Average (SORA) used for floating rate packages moved downwards as well, leading to more favourable borrowing costs and mortgages for Singapore homebuyers.

Locally, this trend has resulted in fixed mortgage rates dropping below 3%, prompting a surge in homeowners opting to refinance their loans. Even so, this trend may not align with earlier, more optimistic forecasts.

Latest Fed projections indicate that there will only be two rate cuts in 2025, down from the four quarter-point cuts forecasted in September last year. This revision comes on the heels of slower progress on inflation and a changing economic outlook with a Trump presidency. Consequently, with higher-for-longer interest rates, SORA rates will see a more measured pace of decline in coming months.

Even so, buyers seeking a new private home may still find it worthwhile to enter the market now, despite expectations of a further (but slower) drop in borrowing costs.

Falling interest rates have historically pushed demand for new homes higher, resulting in growing prices. As such, waiting for further downticks in mortgage rates may not be the most beneficial strategy for aspiring private homeowners.

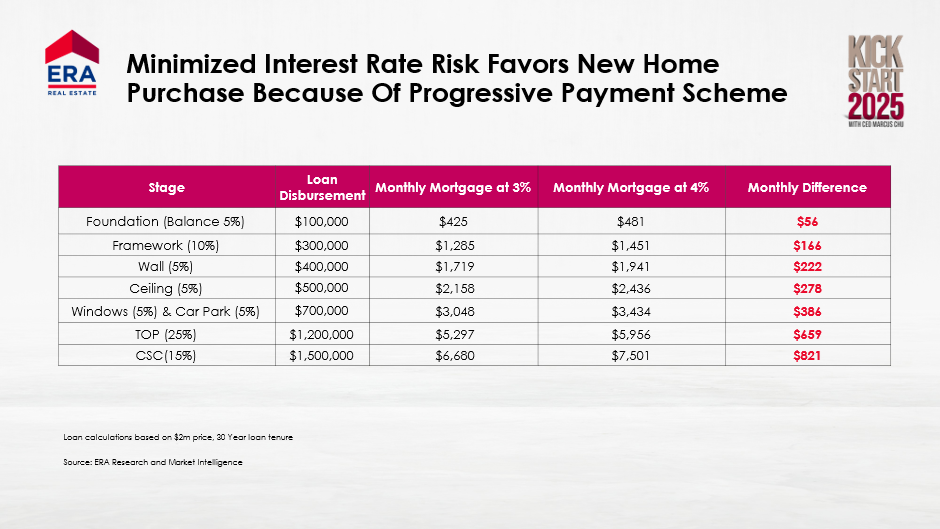

Instead, buyers waiting on the sidelines should capitalise on the Progressive Payment Scheme (PPS) for new private home purchases. With the PPS, interest is levied on funds disbursed at each construction milestone rather than the full loan amount; this helps in easing the financial burden of consumers, especially in high-interest-rate environments.

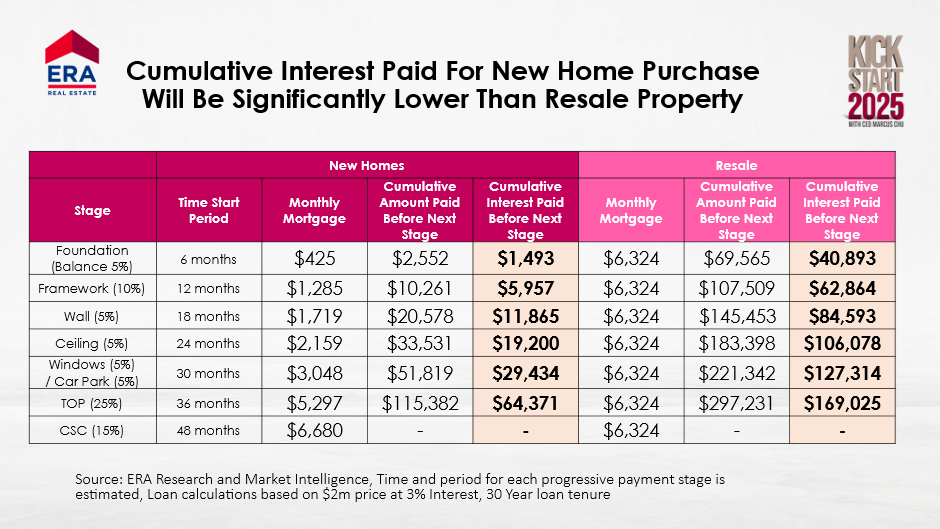

Moreover, the PPS also makes purchasing a new private home more manageable than buying a private property on the secondary market. Similarly, this is due to the lower cumulative interest paid at each stage of construction for new private homes, as compared to a mortgage taken on resale homes where interest accrues on the entire principal from the outset.

Assuming a principal loan amount of $2 million, a mortgage rate of 3%, and a 30-year repayment period, a new home buyer would pay only $1,493 in interest at the six-month mark. In comparison, buyers purchasing a resale private home of equivalent value would have to shoulder $40,893 in interest payments – or put simply, a substantially greater financial load over the same period of time.